A chaotic selloff in the Treasuries market was spurred by a massive exodus from popular trades, heightened by liquidity concerns that could inflict more pain in coming days.

The exodus happened at a time when traders were already worried about the imminent disappearance of a support beam for the market -- a regulatory exemption that has allowed banks to accumulate more U.S. bonds.

Treasury futures open interest across a range of maturities sank by a huge amount Thursday: the equivalent of $50 billion of 10-year notes. It didn’t help that this coincided with the Treasury Department selling $62 billion of seven-year notes, an auction that proved to be a disaster.

The month ahead could be rocky, too. Back in April, the Federal Reserve tweaked its rules to exempt Treasuries from banks’ supplementary leverage ratios -- allowing them to expand their balance sheets with U.S. debt. But that relief ends March 31 and what happens next is something of a mystery.

“It wasn’t an orderly selloff and certainly didn’t appear to be driven by any obvious fundamental continuation or extension of the reflation thesis,” wrote NatWest Markets strategist Blake Gwinn in a note to clients. A number of more technical factors were in the mix, against a backdrop of a good-old-fashioned buyers strike, he said.

WATCH: Pimco’s Geraldine Sundstrom says markets may be getting a little bit rushed into pricing rate hikes.

Source: Bloomberg)

Here’s a look at some of the factors driving Thursday’s moves:

The Protagonist

The main protagonist in the bond market was the five-year Treasury note, a maturity often associated with long-term Fed rate expectations, where yields closed 22 basis point higher on the day. The so-called butterfly-spread index -- a measure of how the note is performing against its two- and 10-year peers -- jumped 24 basis points, the worst daily performance for the sector since 2002.

The selling was triggered after a U.S. auction of seven-year bonds saw record low demand. The bid-to-cover ratio -- a gauge of investor interest -- came in at 2.04, well below the recent average of 2.35. That sent five-year yields surging through 0.75%, a crucial technical level watched by investors as a signal that any bond selloff could worsen.

Unwind Rush

The yield spike sent traders scurrying to manage their positions, in particular those linked to the popular reflation trade. Bets on a steeper yield curve were hit as the curve flattened thanks to heavy losses in shorter-dated bonds.

Preliminary open interest in Treasury futures across the curve -- a measure of outstanding positions -- collapsed by an amount equivalent to $50 billion in benchmark 10-year notes. While there may be some muddiness to the data given potential contract rolls, it does suggest a significant unwind of positions.

| Maturity | Change in number of contracts (net of rolls) |

$m value of 1 basis point move |

|---|---|---|

| TU (2-year) | 591 | 0.27 |

| FV (5-year) | -124,152 | -6.89 |

| TY (10-year) | -174,423 | -14.98 |

| UX (Ultra 10-year) | -50,986 | -6.99 |

| US (Long bond) | -24,158 | -4.72 |

| WN (Ultra bond) | -44,792 | -15.76 |

| Total | -417,920 | -49.61 |

The selloff paused in Asia trading hours and remained calm during Friday in New York. Some Asian traders said they had worked through New York hours right through much of Friday.

The 10-basis-point spike and subsequent retreat in benchmark Treasuries when they touched 1.5% also suggests some traders were hit with stop-losses on their long positions.

Fundamental Decoupling

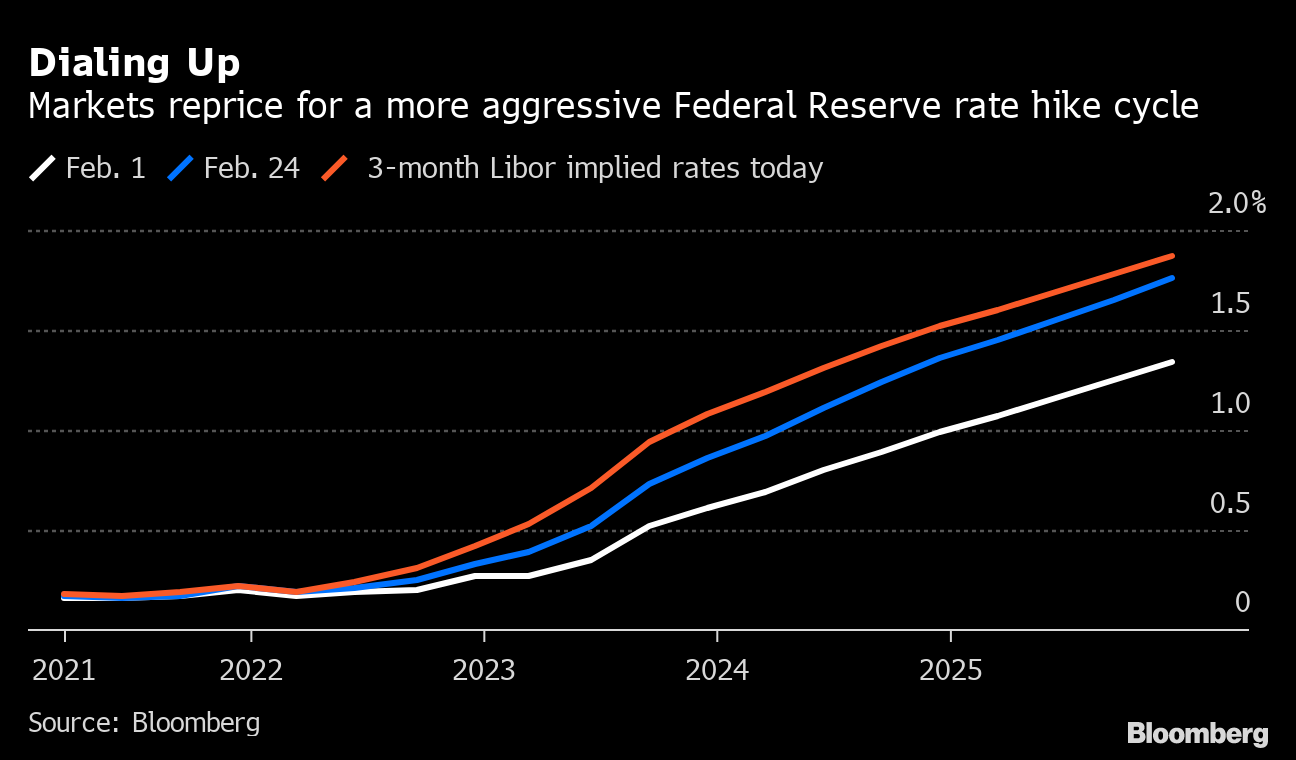

The bond market’s divergence from a fundamental backdrop was most evident at the shorter-end of the curve. Eurodollar contracts -- which are priced off Libor -- collapsed in record volumes as traders repriced their expectations for the path of Fed rates with few obvious catalysts.

Markets now see a Fed hike by March 2023 compared to mid-2023 previously, and have priced in rates over 50 basis points higher by 2024.

Dialing Up

Markets reprice for a more aggressive Federal Reserve rate hike cycle

Source: Bloomberg

But in remarks this week, Fed Chairman Jerome Powell offered reassurance that policy would continue to be supportive and look beyond a temporary pick-up in inflation, especially from a low base. While Fed Vice Chair Richard Clarida expressed cautious optimism on the outlook, he said it would “take some time” to restore the economy to pre-pandemic levels.

“Today’s market dynamics look to have been fueled by technical factors and the Fed may want to let the dust settle before it judges whether there is anything really problematic here,” said Evercore ISI’s Krishna Guha and Ernie Tedeschi. “But a change of tone at least seems warranted in our view and possibly more.”

Liquidity Drought

A lack of bond market liquidity, just when traders needed it most, can also be at fault.

“We think that a steep decline in market depth contributed to the outsized moves in yields,” wrote JPMorgan Chase & Co. strategist Jay Barry in a note to clients. Barry showed how the share of high-frequency traders in the Treasury market -- which has been on an increasing trend -- tends to retreat rapidly as volatility spikes.

U.S. 3-month 10-year swaption volatility -- a gauge of price swings in the rates market -- jumped to highest in over a year on Thursday, having risen steadily all month.

“Given the natural feedback loop between volatility and liquidity, it’s likely that a steep decline in depth contributed to the outsized moves in yields,” added Barry.

Regulatory Purgatory

Bond traders were already on edge as they waited for Fed guidance ahead of next month’s expiry of a regulation that has encouraged banks to buy Treasuries. Neither Powell nor Randal Quarles, the vice chair for supervision, gave an answer as to whether the measure would be extended, which likely helped extend a clearing of positions in the swaps market.

Read more about the significance of the SLR exemption

Credit Suisse strategist Zoltan Pozsar said clarity on this situation is one of the things needed to calm long-term Treasury yields.

No matter what the Fed decides, “both would offer clarity and direction to the rates market,” he said.

— With assistance by Edward Bolingbroke, and Alex Harris