An upstart contender to U.S. Treasuries has emerged in the wake of last month’s vicious debt rout.

Chinese government bonds have defied the turbulence rocking peers from Australia to Europe, offering a port in the global reflation storm. JPMorgan Asset Management and Brandywine Global Investment Management LLC are among those who now see them mimicking the resilience that has afforded U.S. government debt the status of the world’s safest asset in times of crisis.

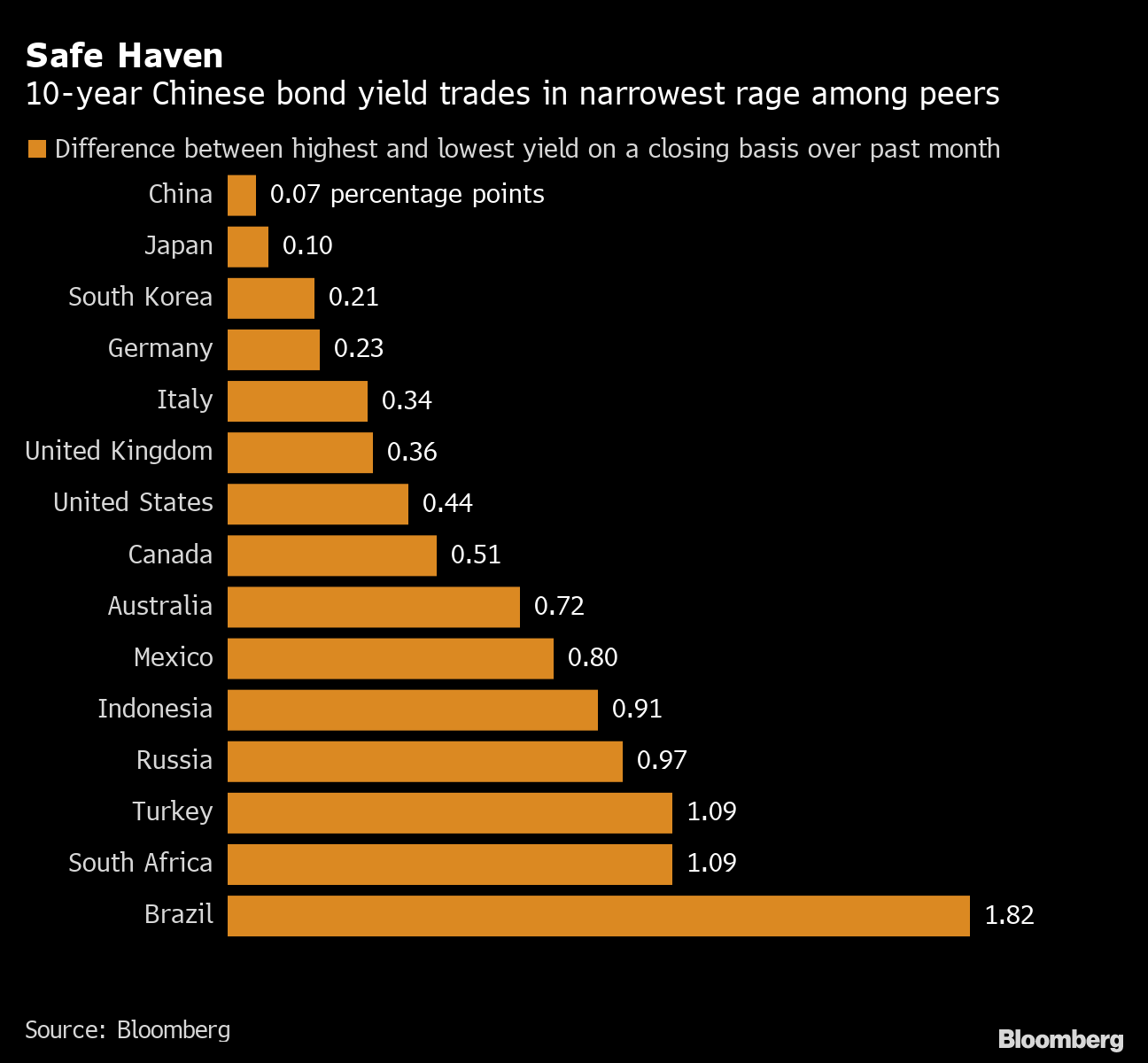

The nation’s 10-year yield has been wedged in a tight eight basis-point range over the past month, even as price swings in the rest of the bond world have broken out. While that doesn’t automatically make Chinese bonds the go-to bulwark against volatility, it helps explain why a market once closed to most international investors is emerging as a shock absorber in wild pandemic trading.

“At times when you’re seeing volatility in the developed markets like you’re seeing now, it’s a good place to keep your cash,” said Arjun Vij, who co-manages JPMorgan Asset Management’s $1.6 billion Global Bond Fund. “China government bonds are as good an asset as U.S. Treasuries when looking at long-term correlations versus global stocks.”

Safe Haven

10-year Chinese bond yield trades in narrowest rage among peers

Source: Bloomberg

Casting Chinese debt as a viable asset class for trillions of dollars in savings is controversial, given liquidity and accessibility issues as well as currency risk. But since it’s only very loosely correlated with other bond markets, it makes for a nifty hedge, the thinking goes, especially when the rest of the world’s biggest bond markets are getting clobbered in tandem.

In New 60/40 Portfolio, Riskier Hedges Are Displacing U.S. Debt

As a sign of just how insulated the market is, the correlation between one gauge of China’s debt and a broader Bloomberg Barclays global aggregate held close to zero during the rout two weeks ago. The relationship is now just 0.2, where a reading of 1 would indicate the two move hand-in-hand and zero means there’s no correlation whatsoever.

That follows a similar pattern during the pandemic turmoil last March where the market was exceedingly stable, defying the storm in U.S. Treasuries.

Alternative Hedge

Holding Chinese debt is an alluring proposition for money managers looking for fresh hedges to counterbalance to their riskier stock holdings, a bedrock of the ubiquitous 60/40 portfolio. It also comes as investors begin to ask serious questions about the plumbing of the Treasury market amid the recent volatility.

“Treasuries’ role as a safe haven is not there anymore,” said Tracy Chen, a Philadelphia-based portfolio manager at Brandywine Global, who bought Chinese debt for the first time last year. “There is an increasing possibility of using China bonds as an alternative.”

China was the first major economy to emerge from the pandemic. As a result, yields there had already risen to levels last seen before the crisis, something bond investors in the rest of the world are only beginning to grapple with. At 3.25%, the yield on China’s 10-year bond now towers over its major peers.

Investors are taking notice. Chinese bonds funds saw $420 million of inflows in the week through March 10, even as investors lowered their emerging-market holdings by the most in nearly a year, according to EPFR Global. They haven’t seen outflows in about 10 months.

Foreign investors bought 93.6 billion yuan ($14.4 billion) worth of Chinese debt in February, after adding positions at a record pace the previous month, egged on by the addition of China’s government and policy-bank bonds into the world’s major indexes in 2019.

“From a relative value perspective, all stars are aligned,” said Jean-Charles Sambor, head of emerging-market debt at BNP Paribas Asset Management in London who is overweight Chinese debt.. “We’re likely to see rotation not only from low yielders in emerging markets but also from global markets into China.”

| What Bloomberg Intelligence has to say: |

|---|

“The low and negative correlation with the U.S. could render China treasuries less susceptible to the possible scenario of a further U.S. Treasury selloff.” - Stephen Chiu, FX and rates strategist in Hong Kong |

Still, there are plenty of risks that can throw a wrench into the trade. China is looking to curb a rapid buildup in financial leverage, which means the central bank may guide borrowing costs higher. The debt market has long been criticized for its poor liquidity since local lenders hold the majority of bonds and don’t actively trade them.

Last Friday, a normally dull Chinese policy-bank bond surged more than 200%, sending the yield to minus 14% by the close. While the move was erased on Monday, concern over what happened will linger.

“China has a lot of work to do in terms of boosting liquidity for investors and build some financial infrastructure to enable people to do futures,” said Brandywine Global’s Chen.

Uneven Field

There’s also the question of the geopolitical rivalry between the U.S. and China that could spill over into the financial sphere, despite optimism that relations would improve under President Joe Biden. Meanwhile, the nation’s capital controls make it an uneven playing field for foreign investors.

To access the market, international funds must wade through rounds of paper work. Once in, they need to navigate local tax policy and don’t have recourse to hedging tools. The central bank also maintains a tight grip on the currency and can often dictate its direction.

In contrast, the $21 trillion Treasury market is still the deepest in the world, with close to $3 trillion changing hands each week on average over the past year. It serves as the benchmark risk-free rate for assets of many stripes. All that means it’s in a class of its own.

Despite the limitations, foreign investors are willing to make sacrifices to get their hands on Chinese debt.

“Every CIO we’re talking to is now making their first allocation to China,” said Hayden Briscoe, head of fixed income for Asia Pacific at UBS Asset Management in Hong Kong. “This is the single largest change in capital markets in anybody’s lifetime.”

— With assistance by Liz McCormick, and Wenjin Lv