China Huarong Asset Management Co. has reached funding agreements with state-owned banks to ensure it can repay debt through at least the end of August, by which time the company aims to have completed its 2020 financial statements, people familiar with the matter said.

The liquidity support, arranged under the guidance of China’s financial regulator, means Huarong can obtain financing from lenders such as Industrial & Commercial Bank of China Ltd. if needed, the people said, asking not to be identified as the matter is private. The distressed debt manager has been effectively shut out of the offshore bond market since the end of March, when it spooked investors by missing a deadline to disclose 2020 results.

Huarong plans to finish its annual report before the end of August, the people said. It’s unclear whether the funding backstop from state banks will be extended beyond that point.

While big questions remain about Huarong’s long-term plans to overhaul its business, the funding arrangement suggests the embattled firm still enjoys near-term financial support from China’s government.

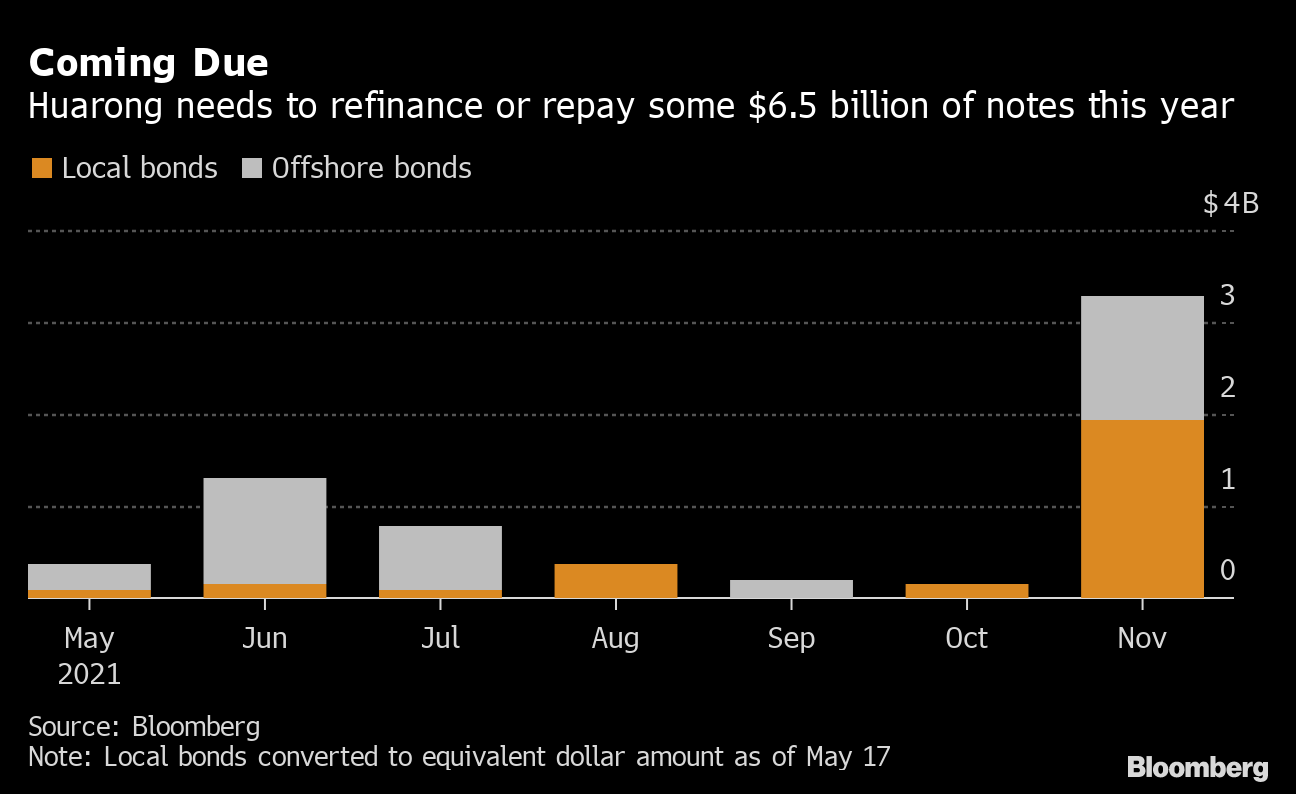

Authorities may be keen to avoid any major market disruptions around the politically sensitive 100th anniversary of the ruling Communist Party on July 1. Huarong has the equivalent of $2.83 billion in offshore and onshore bonds coming due through August, including a dollar bond that matures on Thursday, data compiled by Bloomberg show.

The company has become a closely watched proxy for China’s willingness to backstop government-owned borrowers amid a record wave of corporate defaults. Investors have grown concerned about Huarong’s financial health -- and its level of support from Beijing -- after an ill-fated expansion under former Chairman Lai Xiaomin, who was executed for crimes including bribery in January.

| Read more: |

|---|

Huarong Says No Change in State Support, Ready to Repay Debt Shape of China’s Huarong Resolution Could Depend on Its Size China Huarong’s Journey From Safe Bet to Bad News: A Timeline |

Market sentiment toward Huarong has deteriorated in recent days after Caixin Media’s WeNews reported that the company was urged by regulators to solve its financial issues on its own. While bond prices indicate investors are still betting Huarong will meet its near-term obligations, there’s far less certainty now than before the company’s earnings delay jolted the market.

Huarong’s $400 million bond maturing in July, which traded at par before the delay, is now priced at about 94 cents -- an unusually steep discount for an issuer that’s still considered by the major international ratings firms to be investment grade. The company’s $1.5 billion perpetual bond is trading at about 63 cents, reflecting even bigger doubts about its long-term prospects.

Coming Due

Huarong needs to refinance or repay some $6.5 billion of notes this year

Source: Bloomberg

Note: Local bonds converted to equivalent dollar amount as of May 17

Losses have recently spread from the offshore market to several of Huarong’s bonds onshore. A 2023 note issued by the company’s securities unit plunged 18.8 yuan to 80 yuan on Monday, according to Shanghai fixed-income trading platform prices compiled by Bloomberg. One of the company’s onshore notes due 2022 sank to a record low last week.

Huarong, the China Banking and Insurance Regulatory Commission and ICBC didn’t immediately reply to requests for comment.

Huarong said in a response to questions from Bloomberg last week that it’s prepared to make future bond payments and has seen no change in support from China’s government. The company repaid its S$600 million ($452 million) bond due April 27 with funds provided by ICBC’s Singapore branch, people familiar with the matter said last month.

China’s government has so far been quiet about Huarong’s fate, apart from comments by the CBIRC last month that the company was operating normally and had ample liquidity. Defaults at state-backed firms have increased in recent years as President Xi Jinping dialed back support for weaker borrowers to reduce moral hazard, though none of those that missed payments were as systemically important as Huarong.

The company owes domestic and international bondholders the equivalent of about $41 billion and ranks among the biggest Chinese issuers in offshore markets. It is majority owned by China’s Ministry of Finance and is deeply intertwined with the nation’s $54 trillion financial industry.

Any default by Huarong would undermine a longstanding assumption that China’s government will always step in to help to important state companies in times of trouble.

— With assistance by Charlie Zhu, Jun Luo, Heng Xie, Zheng Li, Dingmin Zhang, and Rebecca Choong Wilkins