Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

As Bank of England officials consider how to unwind their emergency pandemic-era stimulus, markets have already made up their minds about what the first step will be. The conclusion could spell trouble for Chancellor of the Exchequer Rishi Sunak.

Investors are penciling in the BOE’s first 15-basis-point interest-rate hike for September 2022, reversing its last cut, just nine months after the central bank is scheduled to wrap up its latest round of buying, and too soon to have allowed for any significant balance-sheet reduction.

That would have major consequences for Sunak, who has run up the U.K.’s biggest-ever peacetime deficit to fund crisis aid, and relied on BOE stimulus to keep borrowing costs under control.

The BOE slashed rates to 0.1% and more than doubled its asset-purchase target to 895 billion pounds ($1.26 trillion) during the crisis. Now, officials led by Governor Andrew Bailey are discussing whether their previous guidance -- that they’d hold onto to those bonds until interest rates hit 1.5% -- is still suitable.

“The world has changed hugely” since the BOE last reviewed its stance on tightening, Bailey said following the central bank’s May decision. “It’s appropriate to review that again.”

While the review is yet to be completed, Bailey himself last year suggested he was open to a major shift, and was prepared to reduce the institution’s balance sheet before raising interest rates.

Aaron Rock, an investment director at Aberdeen Standard Investments, is holding to the view that rate hikes will precede any reduction of the balance sheet. He expects the BOE to halve the policy rate at which balance sheet reduction will be considered to around 0.75%, a level currently anticipated to be reached only in the second half of 2024.

Flexible Option

However, Rock flagged a risk the review may decide on a more flexible option, allowing the balance sheet to be reduced “starting next year at the same time they are hiking policy rates from 0.1%.”

The BOE’s holdings of bonds are financed at its key interest rate, and the massive expansion of quantitative easing since the pandemic began has left the nation twice as sensitive to a one-point move, according to the Office for Budget Responsibility.

Even a small increase would immediately filter through to debt-servicing costs, with the buying having shortened the median maturity of public debt to less than two years, from more than seven before the financial crisis, according to the OBR.

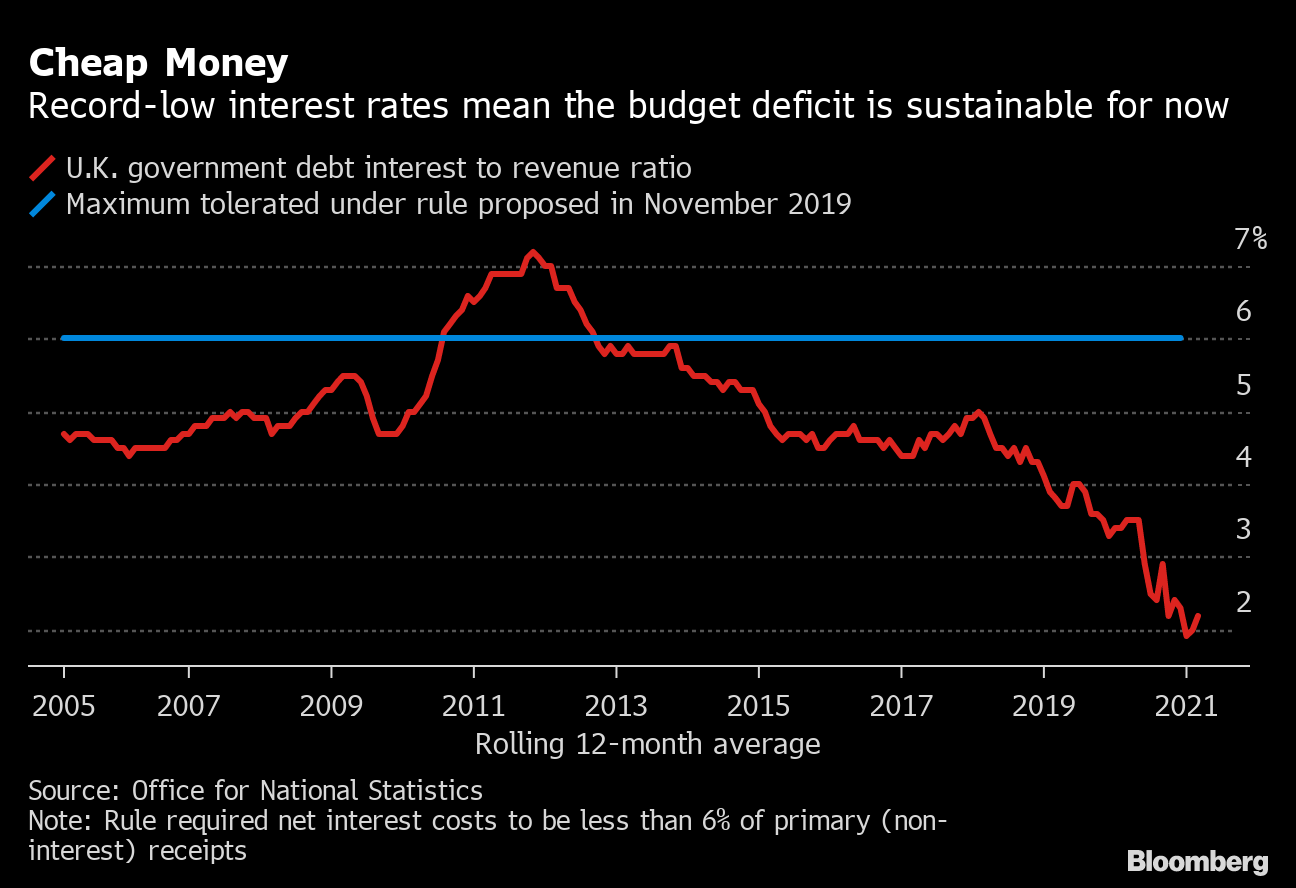

Cheap Money

Record-low interest rates mean the budget deficit is sustainable for now

Source: Office for National Statistics

Note: Rule required net interest costs to be less than 6% of primary (non-interest) receipts

“I still believe that hikes are a long way off,” said Mike Riddell, portfolio manager at Allianz Global Investors. He doesn’t expect the central bank to ever reduce its balance sheet, despite this being its intention a decade ago.

“Now that we have even more debt, which makes the economy even more sensitive to higher rates, then I’d be surprised if the U.K. or global economic backdrop is such that quantitative tightening would be deemed necessary,” Riddell said.

That’s not the view of Goldman Sachs Group Inc., which expects balance-sheet reduction to push the first rate hike out as far as 2025.

“We expect the Monetary Policy Committee to reverse the previous exit sequencing and adopt a ‘last in, first out’ approach for the process of monetary tightening,” wrote Goldman Sachs economists including Jari Stehn.

The Treasury was happy to reap the rewards from QE, so “when the bank begins to tighten policy, it should be prepared to live with the consequences,” Nick Macpherson, former Permanent Secretary at the Treasury, said in a video seminar on Tuesday.